Estimated reading time: 6 minutes

Innovations in Extraction and Recycling

Rare Earth Elements (REEs) have become the invisible backbone of modern technology and a cornerstone of the global economy. These metallic elements, despite their understated name, are critical to everything from smartphones and electric vehicles to renewable energy systems and advanced military applications. Their strategic importance has transformed them into a focal point of international economic policy and geopolitical rivalry.

What Are Rare Earth Elements?

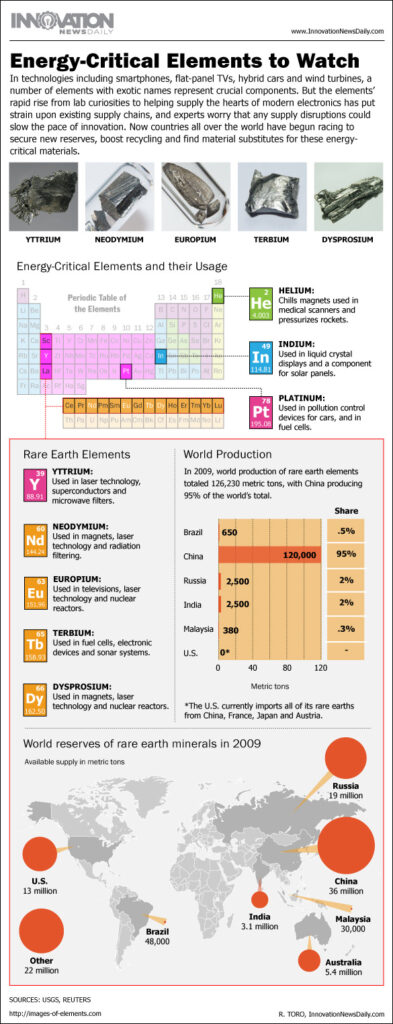

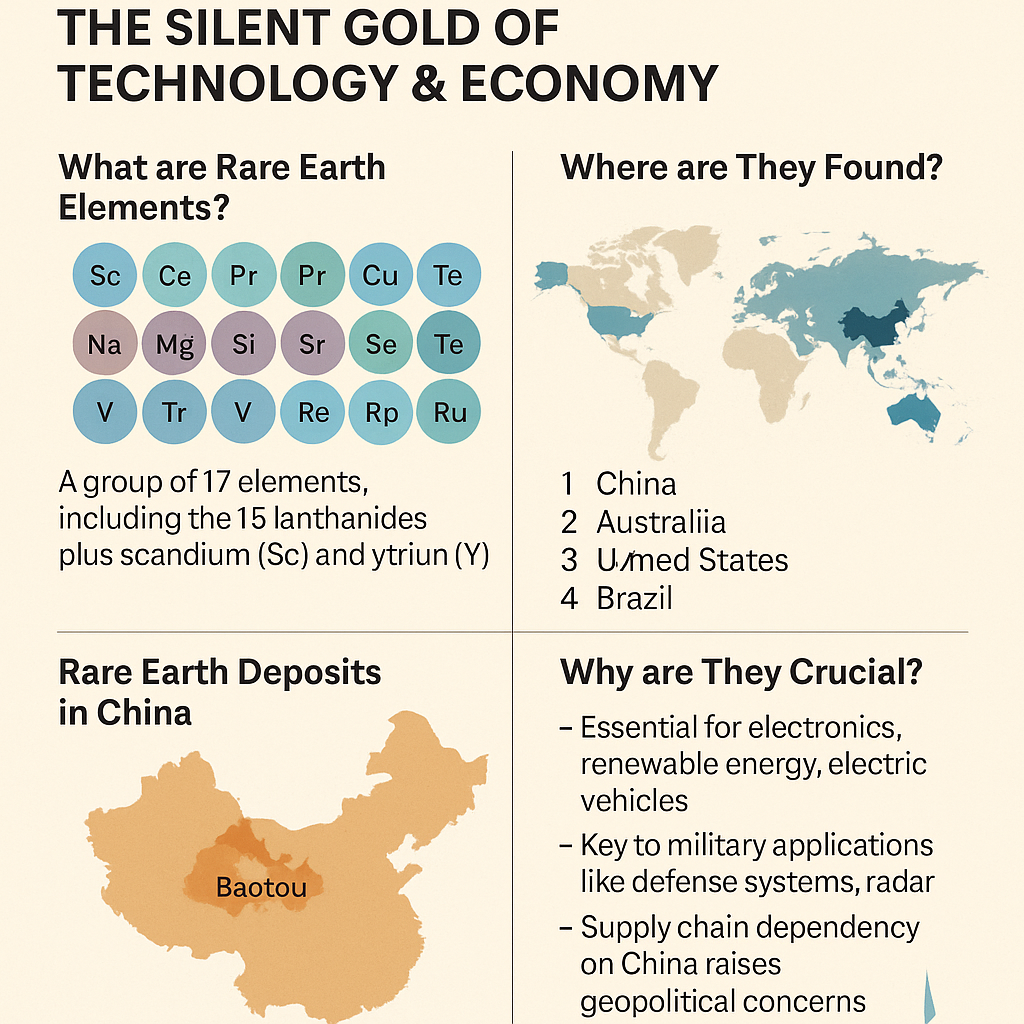

REEs consist of 17 metals: the 15 lanthanides, plus scandium and yttrium. Their exceptional magnetic, luminescent, and electrochemical properties underpin high-performance technologies, including permanent magnets, LED displays, and advanced batteries. While not truly scarce in Earth’s crust, REEs are rarely found in concentrated, economically viable deposits—making their extraction and separation complex and expensive.

Why They Are Considered “Rare”

The term “rare” describes their geological dispersion: REEs tend to occur together in low concentrations, requiring sophisticated chemical processing for separation. Environmental costs are substantial, as mining and refining often produce radioactive waste and toxic by-products—up to 2,000 tons of toxic waste per ton extracted. In 2024, global production reached roughly 390,000 metric tons REO equivalent, with China responsible for nearly 70%.

Global Distribution of Resources

Economically recoverable REE reserves top 90 million tons REO equivalent, with key holders including:

China: Largest reserves (44 million tons) and processing capacity.

India: 6.9 million tons; increasing development.

Australia: 5.7 million tons; major Western supplier.

Thailand: 4.5 million tons; rising production.

Russia, Vietnam, the US, and Greenland: Each with important reserves.

Brazil, South Africa, Tanzania, Canada: Growing significance.

In 2024, world production beyond China included the US (45,000 tons), Burma (31,000), Brazil, Nigeria, Thailand, and Australia (inc. 13,000 each)

China’s Dominance in the Rare Earth Market

China not only leads in mining but also in processing, responsible for 90% of global capacity. Baotou in Inner Mongolia is a major hub. Chinese export controls (tightened in April and October 2025) have caused supply chain disruptions and market volatility. A temporary suspension of some controls was reached with the US in October 2025, but underlying vulnerabilities remain, driving diversification efforts globally.

Economic and Strategic Importance of Rare Earth Elements

REEs are vital to sectors ranging from clean energy (wind turbines, EV motors) and electronics to defense systems (radar, missiles).

Their ubiquity in “technology metals” has prompted national security concerns in the US, Japan, the EU, and others, catalyzing new extraction and recycling projects. US imports in 2024 totaled $170 million (70% from China), with domestic production and recycling initiatives scaling up.

2025 has seen breakthroughs in extraction and recycling technologies:

- Hydrometallurgical Improvements: New solvent agents and membrane separation reduce waste and toxicity while improving recovery rates (85–98% efficiency).

- Bioleaching: Using bacteria to sustainably extract REEs from ores or waste with minimal energy and fewer byproducts (up to 90% recovery from e-waste).

- AI and Automation: Machine learning for process optimization and automated dismantling improves resource yields and lowers costs.

- Urban Mining: Efficiently reclaiming REEs from electronics and industrial waste—recycling could supply up to 25% of global demand by 2035.

- Direct Magnet Recycling: Techniques reduce energy use by 90% over traditional magnets, with comparable performance.

- Membrane/Nanotech Solutions: Target selective extraction with minimal waste, supporting high-purity recovery.

Substitution and Alternative Materials

Research into REE-free technologies is advancing, with iron nitride and manganese aluminum carbide magnets emerging as possible substitutes for neodymium in EVs and wind turbines, reducing environmental impact and supply chain risk. However, these alternatives are still in early stages and present performance challenges.

Environmental and Social Impacts

Mining produces environmental problems: habitat loss, groundwater contamination, high water and energy consumption, and radioactive pollution. Social issues include risks to local health and livelihoods, often in regions with limited regulation. ESG scrutiny is increasing, with new technologies and supply chain transparency measures—like blockchain—for better accountability.

China’s Dominance in the Rare Earth Market

China’s control over the rare earth industry extends far beyond extraction. It dominates processing and refining, handling about 90 percent of the world’s capacity. The Baotou region, often referred to as “the rare earth capital of the world,” hosts massive separation facilities that transform raw ore into refined oxides and alloys. This dominance grants China substantial leverage over global supply chains. When Beijing temporarily restricted exports in 2010 and imposed new controls in October 2025 (affecting technologies for mining, smelting, separation, and related products), it sent shockwaves through global markets. However, as of November 2025, China announced a suspension of some of these rare earth curbs amid ongoing trade negotiations, potentially easing short-term pressures but highlighting ongoing vulnerabilities. These actions have prompted countries like the United States, Japan, and Australia to accelerate diversification, stockpiling initiatives, and investments in alternative sources.

The Geopolitical Dimension

The rare earth sector sits at the intersection of resource economics and geopolitics. The United States and European Union have classified REEs as critical raw materials, essential for industrial resilience. Efforts to diversify supply include reopening mines, investing in refining infrastructure, and forging alliances with resource-rich nations. Japan, for instance, has partnered with Vietnam and India to secure non-Chinese sources. Meanwhile, China’s continued export controls underscore the broader struggle for technological sovereignty in an increasingly multipolar world economy. The U.S. Department of the Interior’s 2025 draft list of critical minerals includes all 17 rare earth elements, emphasizing their role in national security and economic stability.

Challenges and Future Outlook

The sector faces technical, economic, and sustainability hurdles. Recycling is technologically promising but limited by collection, disassembly, and economic viability when market prices are low. Geopolitical uncertainty and regulatory hurdles drive price volatility and strategic stockpiling. Advances in recycling, substitution, and international cooperation offer hope; policy, innovation, and industry investment are shaping a more resilient future supply chain.

Conclusion

Rare Earth Elements are essential to modern technology and global economic strategies, but face significant environmental, technical, and geopolitical challenges. Innovations in recycling and extraction—coupled with policy interventions and emerging substitutes—will be crucial in defining a sustainable, secure future for these “technology metals,” ensuring continued progress in clean energy, defense, and digital infrastructure.

Reference:

- The White House – United States-Japan Framework For Securing the Supply of Critical Minerals and Rare Earths through Mining and Processing – United States and Japan Establish Framework for Securing Critical Minerals and Rare Earths Supply

- Center for Strategic and International Studies (CSIS) – China’s New Rare Earth and Magnet Restrictions Threaten U.S. Defense Supply Chains (October 9, 2025) – China’s New Rare Earth and Magnet Restrictions Threaten U.S. Defense Supply Chains

- MIT Technology Review – 2025 Climate Tech Companies to Watch: Cyclic Materials and its rare earth recycling tech – 2025 Climate Tech Companies to Watch: Cyclic Materials’ Rare Earth Recycling Tech

- Farmonaut – Environmental Impacts of Rare Earth Mining: 7 Challenges – Rare earth elements (REEs) are the unsung heroes powering our modern world. They fueling everything from smartphones and electric vehicles to wind turbines and advanced defense systems.

- Contract Directory – Belt and Road Initiative in 2025: From Silk Road Revival to Green and Digital Expansion