Estimated reading time: 3 minutes

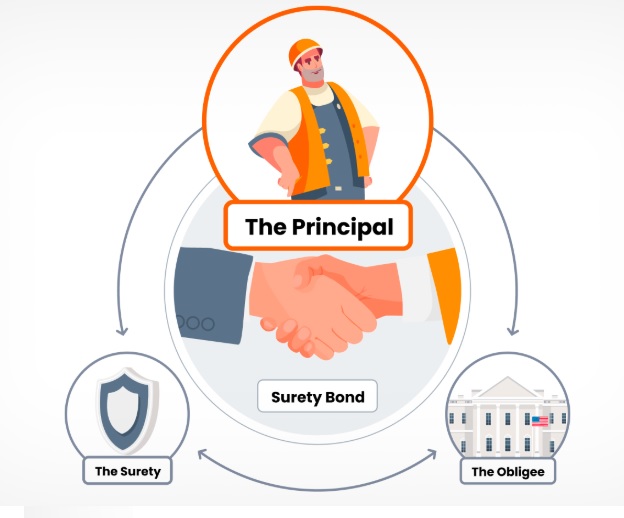

A Surety Bond Agreement is a three-party written agreement by which one party (the Surety) guarantees another party (the Obligee) that a third party (the Principal) will perform according to the bond, statute, contract, or other obligation.

A surety bond is a legally binding agreement between three parties: the principal, the obligee, and the surety. The principal is the party that undertakes to fulfill an obligation, such as completing a project or paying a debt.

The obligee is the entity requiring the bond, often a government agency or project owner seeking protection in case the principal defaults. The surety, usually an insurance or bonding company, assures the obligee that the principal will meet their obligations. If the principal fails, the surety covers the financial loss, but the principal remains liable to repay the surety. This structure ensures confidence and accountability in contractual relationships.

Purpose and Benefits of a Surety Bond

Surety bonds assure that contracted tasks will be completed or that obligations will be met. They protect obligees from financial risks related to non-performance, fraud, or negligence. For example, contractors obtain them to assure clients that projects will be finished as agreed.

Professionals, like auto dealers or mortgage brokers, may need them to obtain licenses or permits. These bonds build trust between parties, reinforce legal compliance, and minimize the risk of financial damage. Therefore, surety bonds play a key role in commercial transactions, public works, and regulated industries.

Types of Surety Bonds

There are several types of contract guarantees, each tailored to different needs. Contract bonds are commonly used in construction and include bid bonds, performance bonds, and payment bonds. These ensure that contractors meet project timelines, quality standards, and subcontractor payments.

Commercial bonds are often required by government agencies to ensure business compliance, such as license and permit bonds. Court bonds are used in legal settings, like fiduciary roles or appeal cases. Despite their different purposes, all surety bonds serve to reinforce trust and reduce exposure to financial risk.

Note: A surety bond in court may be required in situations where financial loss can occur.

Surety Bond vs. Insurance

Although often confused with insurance, a surety bond differs in important ways. Traditional insurance protects the insured, while a bond protects the obligee. In an insurance policy, the insurer assumes the risk. In a surety bond, the principal bears the risk and must reimburse the surety if a claim is paid.

Moreover, insurance premiums are based on pooled risks, whereas a bond premium reflects the principal’s creditworthiness and the specific obligation. While both instruments provide financial assurance, only the surety bond ensures performance and compliance on behalf of another party.

Check out more pages of our website for related content:

Access the Full Contract Directory Index

You can browse the complete alphabetical list of all commercial, financial, and project-based contract templates by visiting our A–Z Contract Index.

References

SuretyBond #FinancialSecurity #ContractGuarantee #ConstructionLaw #BusinessCompliance

has been added to your cart!

have been added to your cart!