Estimated reading time: 3 minutes

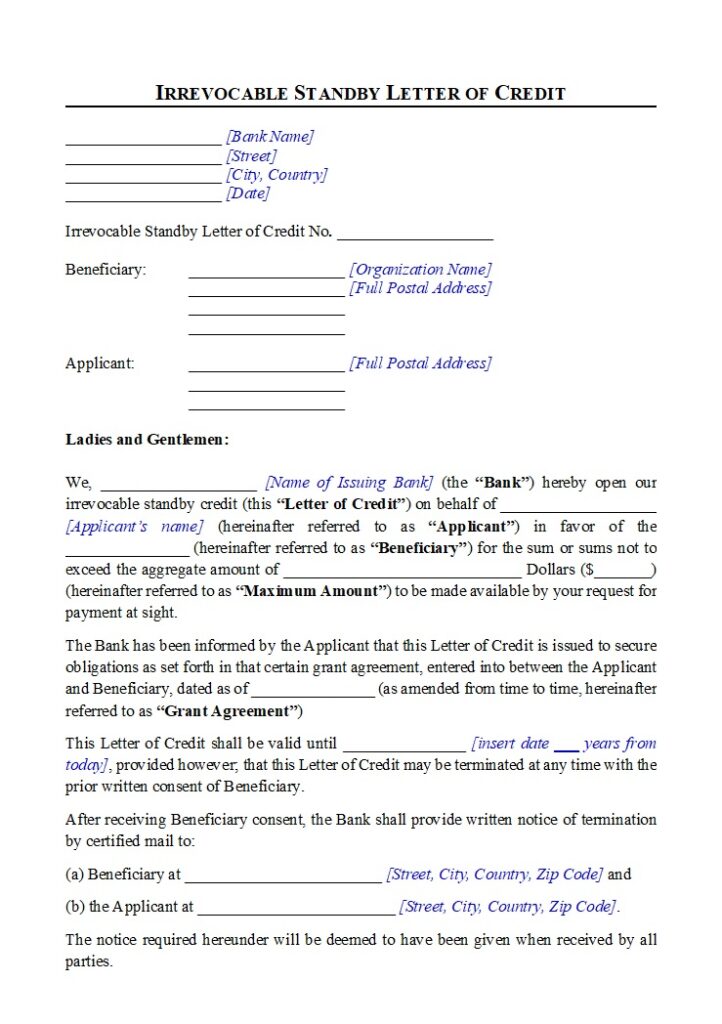

A Standby Letter of Credit (SBLC) serves as a legal and financial guarantee issued by a bank on behalf of its client, known as the applicant. This instrument ensures that a beneficiary receives payment if the applicant defaults on contractual obligations or fails to meet agreed terms. By design, it acts as a safety net that provides trust and stability in international and large-scale transactions.

Purpose and Function of a Standby Letter of Credit (SBLC)

The primary role of an SBLC is to secure payments in case of default. Unlike traditional payment methods, the SBLC does not function as a regular means of transaction but instead as a backstop. Therefore, it becomes enforceable only when the applicant fails to honour obligations. Companies, investors, and traders frequently use this tool to enhance credibility and reduce uncertainty. Furthermore, an SBLC often reassures beneficiaries that financial commitments will be met regardless of the applicant’s financial situation.

Advantages of Using an SBLC

Businesses engaged in international trade face risks such as non-payment, delayed delivery, or breach of terms. By using an SBLC, both parties gain a structured assurance mechanism. Notably, it strengthens negotiations by guaranteeing that obligations will be respected. In addition, it minimizes disputes because the terms are clearly documented within the agreement. Another significant advantage is that the instrument is irrevocable, meaning the issuing bank cannot cancel it unilaterally, which adds further reliability.

SBLC Versus Bank Guarantees

An SBLC shares similarities with a Bank Guarantee since both instruments serve to mitigate risks in large financial or commercial transactions. However, there are nuanced differences. While a Bank Guarantee covers various obligations such as performance, delivery, or payment, an SBLC focuses primarily on ensuring payment in the event of default. Consequently, many traders and project owners prefer SBLCs for transactions where payment certainty remains the key requirement.

Governing Rules and Enforcement

Internationally, SBLCs are governed by the International Chamber of Commerce (ICC) rules, most commonly the Uniform Customs and Practice for Documentary Credits (UCP 600) or the International Standby Practices (ISP98). These frameworks provide consistency and reliability across jurisdictions. Therefore, beneficiaries can rely on standardized enforcement, which reduces legal risks. Moreover, in case of disputes, the SBLC offers straightforward remedies, often enabling beneficiaries to claim payment directly from the issuing bank.

Conclusion

The Standby Letter of Credit stands as one of the most trusted financial instruments for safeguarding transactions. By providing security to beneficiaries and reinforcing the applicant’s credibility, it supports international commerce, large investment projects, and high-value trade agreements. With its irrevocable structure and global acceptance, the SBLC continues to be a cornerstone tool in modern finance.

Check out more pages of our website for related content:

- Standby Letter of Credit (SBLC) – 1

- Standby Letter of Credit (SBLC) Application Form

- Everything About Letter of Credit

Access the Full Contract Directory Index

You can browse the complete alphabetical list of all commercial, financial, and project-based contract templates by visiting our A–Z Contract Index.

Reference:

- Investopedia – Standby Letter of Credit (SLOC): Definition, Benefits, and Process – The article defines a standby letter of credit as a bank’s guarantee of payment to a third party if its client fails to fulfill a contractual obligation, while covering its benefits and operational process.

- Corporate Finance Institute – Standby Letter of Credit (SBLC) – Overview, How It Works, Types – This resource provides an overview of a standby letter of credit as a legal document where a bank guarantees payment of a specific amount to a seller if the buyer defaults, including its mechanics and variations.

has been added to your cart!

have been added to your cart!