Estimated reading time: 2 minutes

A Personal Loan Agreement is a binding document that outlines the terms between a lender and a borrower. It ensures transparency, protects both parties, and defines repayment obligations. This article explains the essential elements of a Personal Loan Agreement and why it is important.

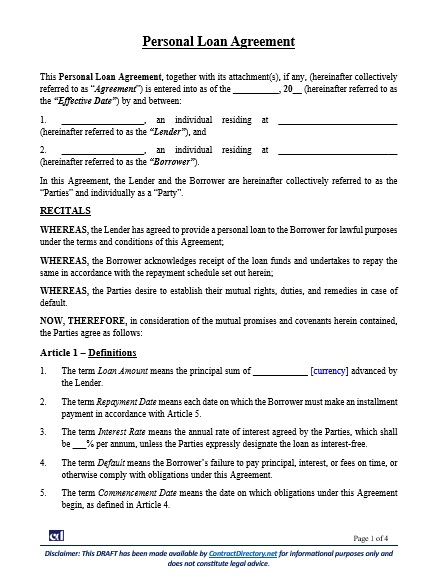

The agreement typically begins with clear definitions of key terms, including the loan amount, repayment schedule, interest rate, and default provisions. It specifies how and when the funds are disbursed, the repayment method, and conditions for prepayment. These clauses establish clarity and prevent ambiguity.

Interest, Fees, and Security Provisions

The agreement details whether the loan is interest-bearing or interest-free. Interest rates, calculation methods, and late payment penalties are included to protect the lender. If security is provided, the type of collateral and enforcement rights are outlined. These terms safeguard the lender’s investment while ensuring the borrower understands potential consequences.

Default and Dispute Resolution

Default clauses outline the circumstances under which the borrower is considered to be in breach, such as missed payments or insolvency. Remedies may include demanding full repayment, enforcing collateral, or pursuing legal action. Dispute resolution mechanisms, like negotiation, mediation, or arbitration, are included to avoid prolonged conflicts and provide a structured path to resolution.

Legal Importance and Confidentiality

A Loan Agreement is governed by the chosen jurisdiction’s laws, making it enforceable in court. Confidentiality provisions ensure that personal and financial details remain protected. Together, these elements make the Agreement a vital tool for financial transactions.

Check out some other pages of our website for related content:

References

has been added to your cart!

have been added to your cart!