Estimated reading time: 2 minutes

A Payment Bank Guarantee secures financial obligations in commercial and construction contracts. The buyer’s bank issues this guarantee in favour of the seller. It assures the seller that payment will occur even if the buyer defaults. The guarantee strengthens trust and enables smooth cross-border or high-value transactions.

Purpose and Function of a Payment Bank Guarantee

The main purpose of a Payment Bank Guarantee is to reduce payment risk. It protects the seller against non-payment while allowing the buyer to trade with extended terms. When the buyer fails to pay, the bank covers the guaranteed amount on demand. This function gives sellers confidence to deliver goods, services, or works without hesitation.

Provisions

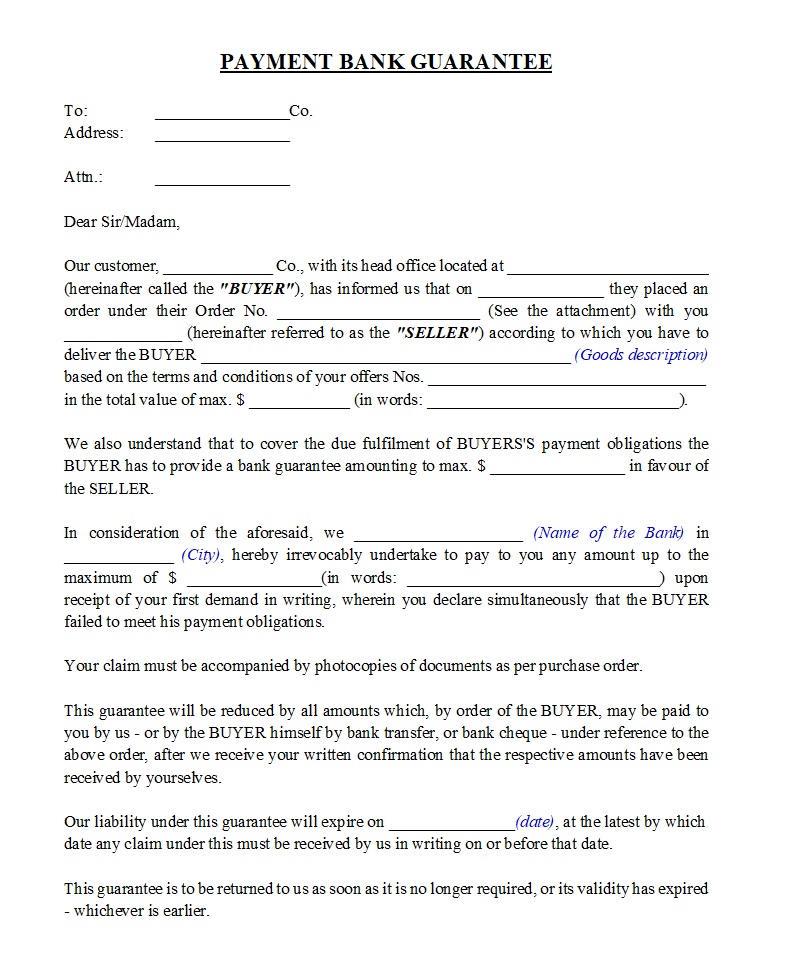

The guarantee document names the buyer as applicant, the seller as beneficiary, and the bank as guarantor. It specifies the guarantee amount, validity period, and claim procedure. It often requires the seller to present a simple written demand for payment. Conditions may also include presenting unpaid invoices or proof of contract breach. The guarantee usually works as an irrevocable and unconditional obligation, giving the beneficiary strong security.

Practical Considerations

Parties should confirm that the guarantee complies with international banking rules such as ICC URDG 758. Sellers must check that the wording avoids unnecessary conditions that delay claims. Buyers should negotiate limits on the guarantee amount and duration to control exposure. Banks assess the buyer’s creditworthiness before issuing, often requiring collateral or credit facilities. Both parties should align the guarantee’s validity with the contract’s payment schedule. Once obligations are finished, the seller must return the guarantee to the bank.

Final Note

A Payment Bank Guarantee plays a critical role in managing payment risk in commercial and construction transactions. When parties structure it carefully and align it with the underlying contract, the guarantee promotes confidence, supports performance, and reduces disputes. Clear wording, proper validity periods, and compliance with international banking standards ensure that the guarantee functions as a reliable financial security rather than a source of uncertainty.

Check out more pages of our website for related content:

- Payment Bank Guarantee (BG) – 2

- Performance Bank Guarantee – PBG

- Uniform Rules for Demand Guarantees (URDG 758)

References:

- Trade Finance Global

- Wikipedia – Bank Guarantee

- General Credit Finance and Development Limited – What You Need to Know About Bank Guarantees 2025

has been added to your cart!

have been added to your cart!