Estimated reading time: 2 minutes

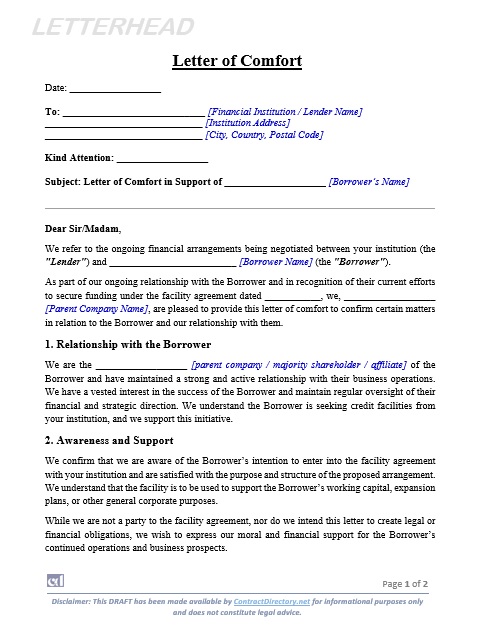

A Letter of Comfort (LoC) offers assurance from a third party to support a borrower. Usually, a parent company issues this letter to help the borrower get credit facilities.

Although the issuer does not take on legal responsibility, it shows moral support. Therefore, lenders gain some confidence to proceed with the loan. Meanwhile, the borrower enjoys improved credibility during negotiations.

This letter uses soft language and avoids strong financial commitments. For instance, phrases like “we expect the borrower to fulfill obligations” are common. However, this vagueness also creates legal ambiguity in enforcement.

Common Uses of a Letter of Comfort

Banks often require some form of assurance when lending large amounts. Instead of formal guarantees, businesses provide an LoC. It supports subsidiaries or related companies in loan transactions. In cross-border financing, LoCs help overcome jurisdictional gaps.

Companies also use LoC during corporate deals or trade finance. As a result, they reduce lender hesitation and smoothen due diligence processes.

Letter of Comfort vs. Guarantee

The Letter differs from a guarantee in its legal power. A guarantee creates a binding obligation on the issuer. In contrast, an LoC contains no enforceable promise to repay.

This difference matters in dispute resolution and financial risk analysis. Even though both offer support, only one binds the issuer by law.

Legal Standing and Limitations

Generally, courts do not treat LoCs as legally binding. However, wording and context can influence court interpretations. Therefore, companies must draft these letters with caution. They should involve legal experts to avoid unintended liabilities.

In summary, the Letter acts as a moral backing tool. It sits between a casual promise and a formal financial guarantee.

Check out another page of our website for related content:

References

- Investopedia – “Letter of Comfort: Definition, Uses, Vs. Guarantee”

- Corporate Finance Institute (CFI) – “Comfort Letter”

- Sprintlaw UK – “Letter of Comfort in the UK: What to Know”

has been added to your cart!

have been added to your cart!